How to Record Personal Expenses in Your Accounting System: Company vs. Sole Trader

Published March 19th, 2026 | Team Gimbla

Mixing business and personal expenses is a common hurdle for small business owners. Whether it happens by accident—like using the wrong bank card at the grocery store — or out of necessity, knowing how to properly record these transactions in your accounting system is crucial. Incorrect bookkeeping can lead to messy financial reports, compliance issues, and headaches during tax season.

The way you code personal expenses in your Chart of Accounts depends entirely on your business structure. Below, we break down exactly how to handle personal expenses for both Registered Companies and Sole Traders.

If you are still deciding how your entity should be set up, start with Which Business Structure Is Right for Your Business?.

Using a robust accounting software like Gimbla makes it incredibly easy to categorise your transactions, keeping your personal and business finances perfectly organised.

1. Recording Personal Expenses for a Company

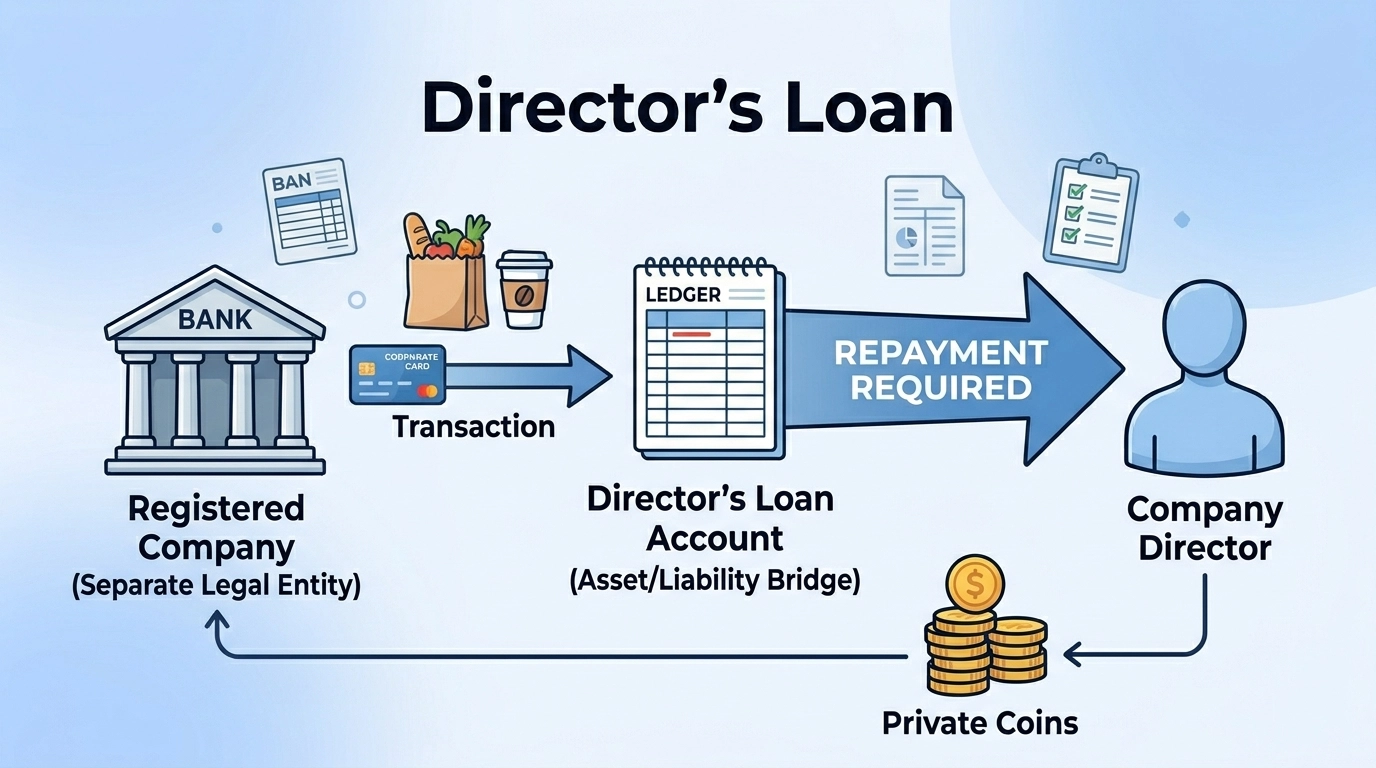

If your business is structured as a registered company (e.g., Pty Ltd, LLC, or Ltd), the business is considered a completely separate legal entity from you, the owner. Because of this legal separation, any company funds used for personal expenses are not simply “yours” to take — they are legally viewed as money the company has lent to you, and it must be paid back.

If the payment is meant to remunerate a company director rather than fix a personal expense, use the guide to director salary and directors’ fees before treating the transfer as a loan. If the payment relates to a vehicle, compare whether it should be a company car or personally owned car before coding it as an ordinary expense.

The Best Account to Use: Director’s Loan (or Due to/from Director)

When a personal expense is paid for using company funds, it should be coded to a Director’s Loan or Shareholder Loan account. For the broader cleanup workflow, read the guide to director loan accounts in Australia.

- Account Type: Current Asset (if the director owes the company) or Current Liability (if the company owes the director).

- Why this is the best account: Coding personal expenses to a Director’s Loan account correctly logs the transaction as a debt owed back to the company rather than a business expense. This ensures your Profit and Loss (P&L) statement remains accurate and strictly reflects business operations. Furthermore, tax authorities monitor personal use of company money closely (such as Division 7A in Australia); recording it as a loan ensures you remain legally compliant and avoid triggering unexpected fringe benefits taxes.

Example Scenario: You accidentally use your corporate credit card to pay for a $200 personal family dinner.

- The Fix: In your accounting system, categorise that $200 bank feed transaction to the “Director’s Loan” account. Later, when you transfer $200 from your personal bank account back into the company to repay it, you will code that incoming deposit to the exact same “Director’s Loan” account, zeroing out the balance.

Once you post the transaction, it will usually appear on your balance sheet rather than as a true operating expense.

2. Recording Personal Expenses for a Sole Trader

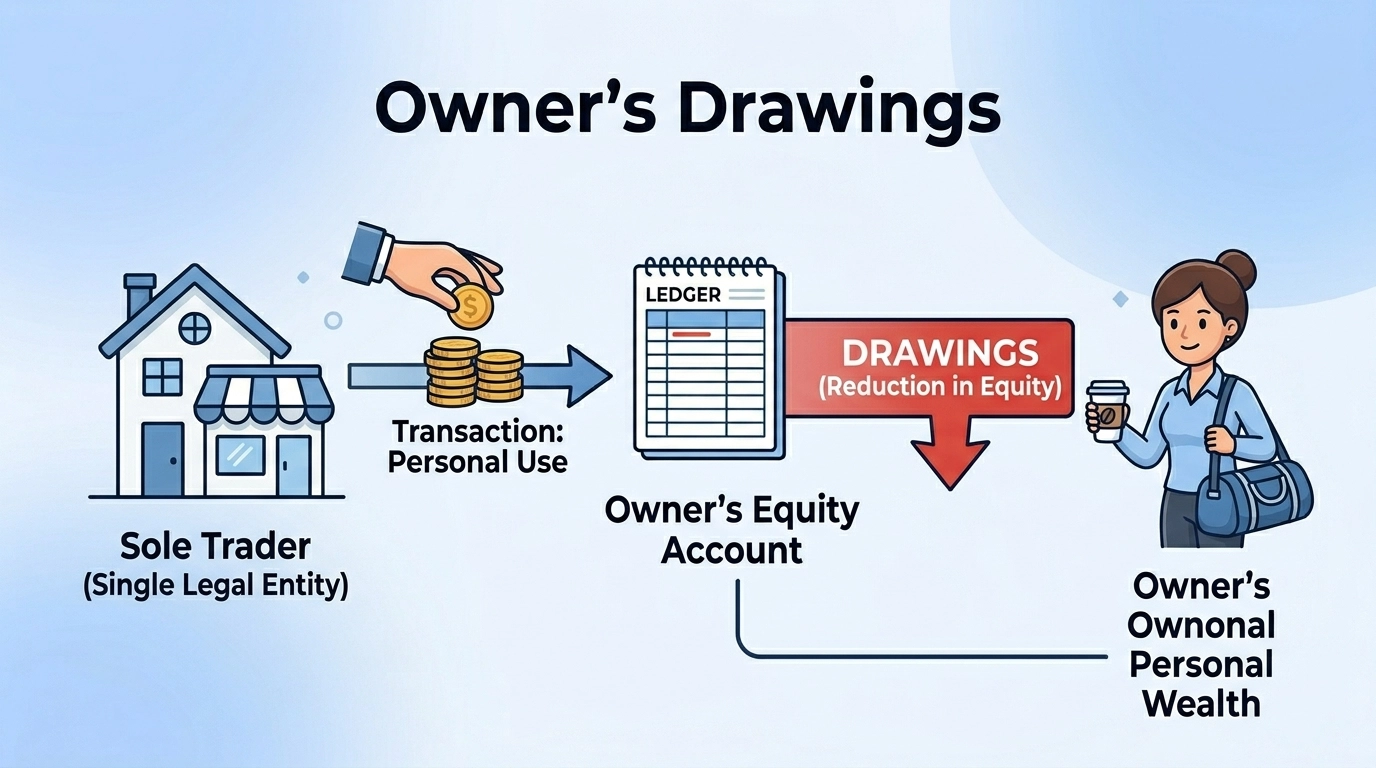

If you operate as a Sole Trader (or Sole Proprietor), the rules are different. Legally, you and your business are the same entity. There is no legal separation between your personal money and your business money, meaning you don’t “owe” the business anything if you spend its funds. However, for the sake of clear bookkeeping and calculating accurate business profits, you still need to separate these transactions.

The Best Account to Use: Owner’s Drawings (Equity)

For a sole trader, personal expenses paid from a business account should be coded to an Owner’s Equity account, specifically named Owner’s Drawings (or Owner’s Personal Use).

- Account Type: Equity

- Why this is the best account: Equity represents your financial interest in the business. When you take money out for personal use, you are simply “drawing” upon your own equity. It doesn’t affect your business’s net profit on the Profit & Loss statement; instead, it correctly appears on your Balance Sheet as a reduction in your overall business equity.

Practical Examples for Sole Traders:

- Example 1 (Owner’s Drawings): You pay for a $50 personal gym membership using your business debit card.

- The Coding: Code the $50 withdrawal to Owner’s Drawings (Equity account). Since it is not a business expense, there is no GST/tax to claim.

- Example 2 (Funds Introduced): You use $100 of your own personal cash to buy printer ink for the business.

- The Coding: You can code the business expense (Office Supplies) and balance it by coding the payment source to Funds Introduced or Owner’s Contribution (another Equity account). This shows you injected personal wealth into the business to cover a legitimate business expense.

If you want a cleaner process going forward, connect your feeds first with the guides for adding a bank account or credit card and bank reconciliations.

Conclusion

Keeping your books clean means understanding the boundaries between your personal and business finances. If you run a company, remember that personal expenses are a loan that must be repaid, strictly tracked via a Director’s Loan account. If you are a sole trader, personal spending simply reduces your stake in the business, easily managed through Owner’s Equity.

By applying these Chart of Accounts best practices within your accounting software, you will streamline your tax preparation, maintain crystal-clear financial reports, and keep your accountant happy!

You may also find these helpful: