Singapore CIT Rebate and Cash Grant: YA 2026 Bookkeeping Checklist

Published June 4th, 2026 | Team Gimbla

Singapore’s enhanced Corporate Income Tax (CIT) Rebate and CIT Rebate Cash Grant for Year of Assessment 2026 are useful cash-flow support, but they still need clean bookkeeping. A company should know whether it is eligible for the cash grant, keep CPF and IRAS evidence, avoid including the rebate in taxable income, and reconcile the Notice of Assessment against the accounts.

For a small business owner or bookkeeper, the practical job is not to calculate a clever tax position. It is to keep the tax computation, IRAS notices, bank movement and supporting records clear enough for the accountant to review.

Treat the YA 2026 CIT Rebate as tax relief to reconcile, not as ordinary sales income. Keep the IRAS notice, CPF evidence and bank record close to the tax working paper.

Quick answer

For YA 2026, IRAS says the enhanced CIT Rebate is 50% of corporate tax payable and the enhanced CIT Rebate Cash Grant is S$2,000. The total maximum benefit from the rebate and cash grant is S$40,000 per company. The IRAS CIT rebate guidance also says the cash grant is for active companies that meet the local employee condition.

The measure was enhanced after Singapore’s 7 April 2026 support update. The gov.sg Budget 2026 page summarises the increase to a 50% CIT rebate, the S$2,000 minimum benefit for eligible companies, and the S$40,000 cap.

For filing, do not add the rebate to chargeable income. IRAS says chargeable income declared in Estimated Chargeable Income (ECI) and in Form C, Form C-S or Form C-S (Lite) should not include the CIT Rebate, because IRAS computes the rebate automatically in the YA 2026 tax assessment.

Key points

- This is a Singapore-specific corporate tax measure for YA 2026.

- The CIT Rebate is based on corporate tax payable, while the cash grant has active-company and local-employee conditions.

- IRAS says the cash grant is not taxable.

- The cash grant may not appear on the ECI or return acknowledgement page, so the Notice of Assessment matters.

- Good records reduce confusion between tax relief, ordinary revenue, GST, bank deposits and income tax payable.

What changed for YA 2026

The headline change is the enhancement from the original Budget 2026 support level. For bookkeeping, the important items are the rate, cap, cash grant amount and evidence.

| Item | YA 2026 position | Bookkeeping implication |

|---|---|---|

| CIT Rebate | 50% of corporate tax payable, subject to the cap and cash grant interaction | Reconcile it against the Notice of Assessment rather than treating it as sales income. |

| CIT Rebate Cash Grant | S$2,000 for active companies that meet the local employee condition | Keep CPF and employee-condition evidence with the tax working paper. |

| Total benefit cap | S$40,000 per company | Ask your accountant to check the cap if the tax payable is high. |

| Automatic processing | IRAS computes the rebate from YA 2026 ECI or Form C/Form C-S/Form C-S (Lite) | Do not manually add the rebate to chargeable income or ordinary income. |

| NOA review | The cash grant is reflected in the Notice of Assessment, not necessarily on the acknowledgement page | Compare the NOA with the tax payable and any bank movement before closing the month. |

Who should check eligibility

The CIT Rebate applies to taxpaying companies for YA 2026, whether tax resident or not, subject to the detailed IRAS rules. The cash grant is narrower. IRAS says a company must be active and must have met the local employee condition.

In plain terms, check:

- whether the company is active at the point of cash grant disbursement

- whether it made CPF contributions for at least one local Singapore citizen or permanent resident employee in calendar year 2025

- whether shareholder-directors are excluded from the employee count

- whether secondment or centralised hiring arrangements need extra supporting documents

- whether a business trust or variable capital company has its own fact pattern to review

This is where payroll and bookkeeping records overlap. A company may think of the rebate as a tax item, but the cash grant condition can depend on payroll evidence. Keep CPF contribution support and employment-cost recharge documents where relevant.

CIT rebate is not the same as ordinary income

The CIT Rebate reduces tax payable. The cash grant is a government support payment connected to the rebate rules. Neither should be buried inside ordinary customer sales.

That distinction matters because customer sales affect revenue trends, margins, GST where applicable, and the Profit and Loss. A tax rebate or cash grant should stay traceable to the tax assessment, bank receipt and accountant working paper.

If the amount is posted to a generic income account, management reports may make the month look stronger than it really was. If it is posted only as a bank receipt with no note, the accountant may need to unwind it later.

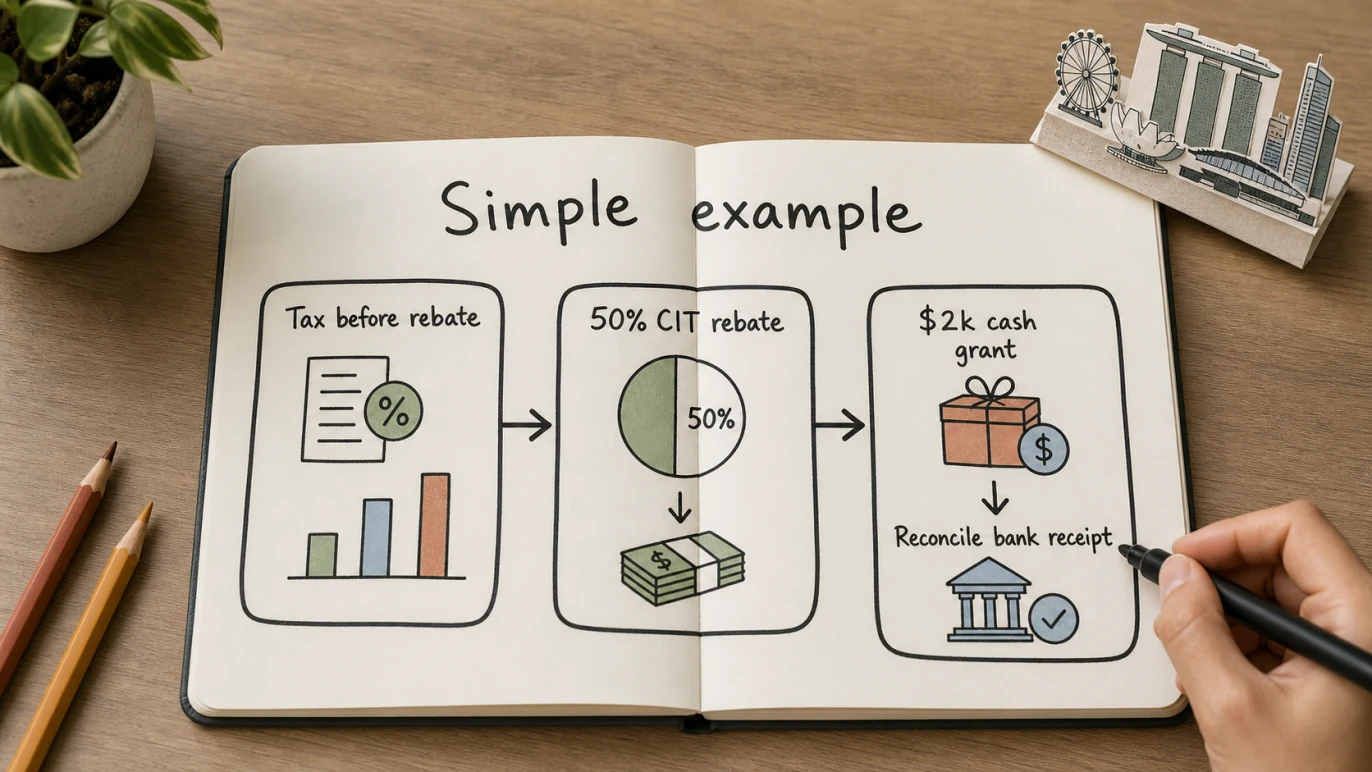

Simple example

A Singapore consulting company has S$12,000 of corporate tax payable before the YA 2026 CIT Rebate. It is active and meets the local employee condition, so it is also eligible for the S$2,000 cash grant.

| Review item | Amount |

|---|---|

| Tax payable before rebate | S$12,000 |

| Computed 50% CIT Rebate benefit | S$6,000 |

| CIT Rebate Cash Grant | S$2,000 |

| CIT Rebate applied against tax after cash grant interaction | S$4,000 |

| Tax payable to reconcile before other credits or payments | S$8,000 |

The accounting review is simple: keep the NOA, note the S$4,000 tax reduction, keep the S$2,000 cash grant support, and reconcile any bank receipt separately. Do not describe the S$2,000 as customer revenue, and do not include the rebate in chargeable income.

Records to gather before relying on it

IRAS says companies must keep proper records of financial transactions, source documents, accounting records, schedules, bank statements and other business transaction records for at least five years from the relevant YA. The IRAS record keeping requirements also say companies should be able to explain transactions relating to income, expenses and purchases.

For this rebate and cash grant, gather:

- YA 2026 ECI acknowledgement, if filed

- Form C, Form C-S or Form C-S (Lite) filing support

- tax computation and accountant working paper

- Notice of Assessment and any amended NOA

- CPF contribution records for the local employee condition

- employee, secondment or recharge documents where the fact pattern is not straightforward

- bank statement line for any cash grant received

- journal note explaining how the rebate and cash grant were treated

This is also a good time to check the company’s broader working capital position. A tax relief item may help cash flow, but it is not a substitute for collecting invoices, paying suppliers on time or reviewing upcoming tax liabilities.

How it fits with Singapore tax filing

Companies still need to report actual income through Form C, Form C-S or Form C-S (Lite). The IRAS overview of Form C-S, Form C-S (Lite) and Form C explains the filing types and the records companies should prepare, even where supporting documents are not submitted with the simplified return.

The key filing habit is separation:

- Prepare the tax computation before rebate.

- File the ECI or corporate income tax return based on chargeable income.

- Let IRAS compute the CIT Rebate automatically.

- Compare the NOA with the expected rebate and cash grant treatment.

- Record the final tax payable, tax relief and cash receipt in a way your accountant can trace.

If the company has concessionary-rate income, withholding tax, tax set-offs or group structures, get tax advice before relying on a simple example.

How Gimbla can help

Gimbla helps small businesses keep invoices, bills, bank reconciliation, reports and supporting notes close to the transaction trail. That matters when a tax relief item appears because the cash movement should connect back to the source evidence.

For a Singapore business, start with free accounting software for Singapore if you need the product context. For the related GST e-invoicing change, see the GST InvoiceNow Singapore guide.

Inside the books, use a clean workflow:

- keep the IRAS notice as an attachment or supporting record

- record any cash grant separately from ordinary sales

- reconcile the bank receipt during bank reconciliation

- review income tax payable before month end

- keep a note in the audit trail if an adjustment is made after an amended NOA

Checklist before month end

Before you close the month or hand records to your accountant, check:

- Has the company confirmed whether it meets the local employee condition?

- Is the tax computation prepared before the CIT Rebate?

- Is the NOA saved with the tax working paper?

- Is any cash grant bank receipt matched to the right account?

- Has the rebate been kept out of ordinary sales revenue?

- Are CPF and employment support records available if IRAS queries eligibility?

- Do directors understand that cash-flow support is not the same as recurring revenue?

FAQs

What is the Singapore CIT Rebate for YA 2026?

IRAS says the enhanced YA 2026 CIT Rebate is 50% of corporate tax payable. The total benefit from the rebate and cash grant is capped at S$40,000 per company.

Who can receive the S$2,000 CIT Rebate Cash Grant?

The company generally needs to be active and meet the local employee condition. IRAS links that condition to CPF contributions for at least one local Singapore citizen or permanent resident employee in calendar year 2025, excluding shareholders who are also directors.

Should the CIT Rebate be included in ECI or Form C-S?

No. IRAS says chargeable income declared in ECI and in Form C, Form C-S or Form C-S (Lite) should not include the CIT Rebate because IRAS computes it automatically.

How should small businesses prepare their records?

Keep the NOA, CPF support, tax computation, bank record, accountant notes and any adjustment working paper together. The goal is to make the rebate and cash grant easy to trace without mixing them into sales or GST records.

In short

The YA 2026 Singapore CIT Rebate and Cash Grant can help cash flow, but the bookkeeping still needs discipline. Keep the rebate out of ordinary income, save the eligibility evidence, reconcile the NOA and bank movement, and ask your accountant to review the final tax treatment before year end.