ATO Interest Charges Are No Longer Deductible

Published May 22nd, 2026 | Team Gimbla

ATO interest charges are more expensive for Australian small businesses than they used to be. From 1 July 2025, general interest charge (GIC) and shortfall interest charge (SIC) incurred on or after that date are no longer deductible in an income tax return.

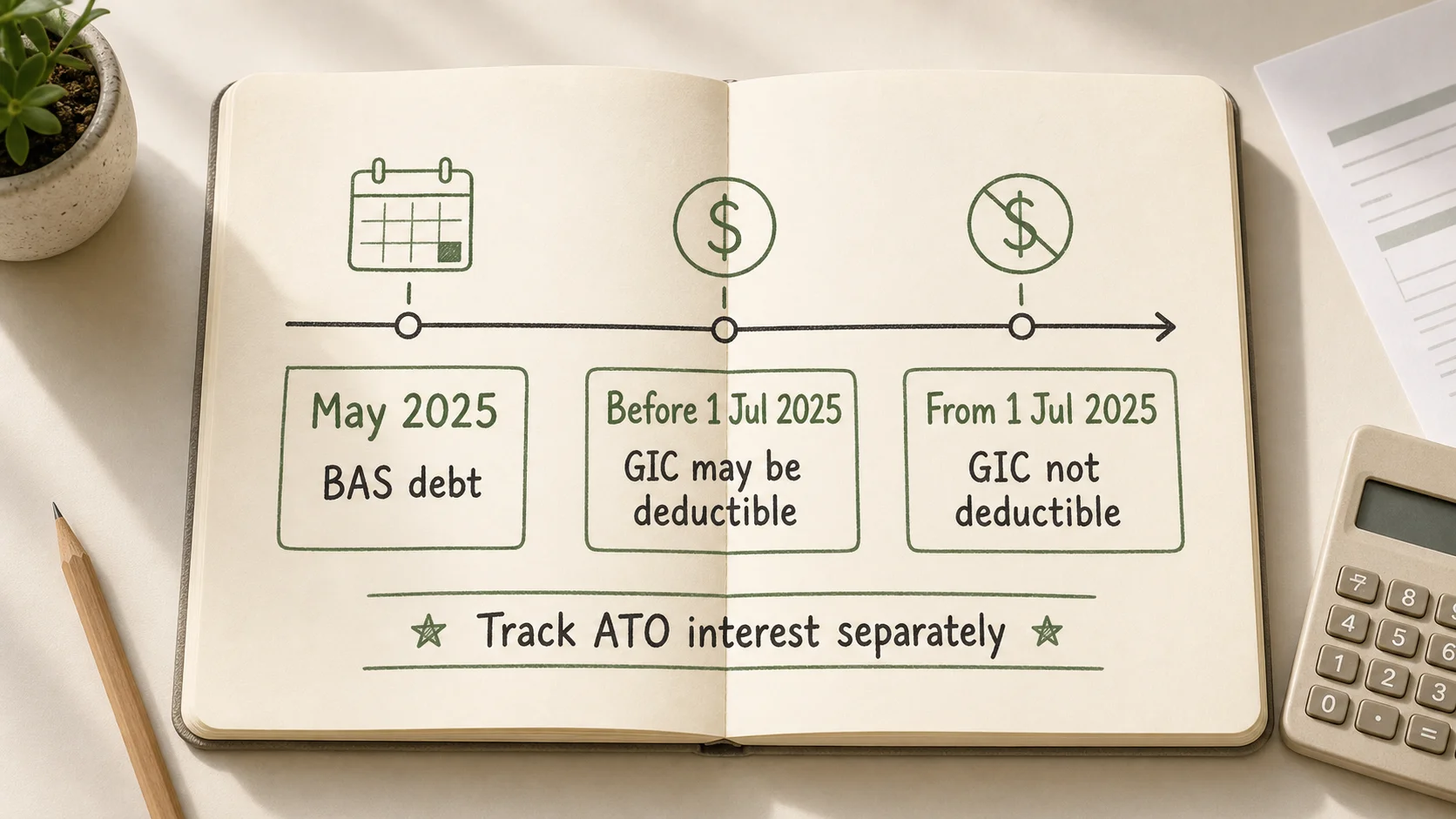

That does not mean every old ATO interest amount changed overnight. It means the incurred date matters. A tax debt from an earlier year can still generate non-deductible GIC after 1 July 2025, so business owners need clean records, careful coding and adviser review before treating ATO interest as a normal expense.

ATO interest is now a cash-flow cost and a bookkeeping accuracy issue. Do not let it disappear into a generic interest or bank-fee account without checking the date and treatment.

Quick answer

The ATO says taxpayers can no longer deduct GIC and SIC incurred on or after 1 July 2025. Its guidance on interest charged by the ATO also says GIC and SIC incurred before 1 July 2025 can be claimed in the income year in which they were incurred.

For small businesses, the practical step is to separate ATO interest from ordinary loan interest, penalties, GST, PAYG and BAS payments. Ask your accountant or registered tax agent how to code any GIC or SIC, especially if the charge straddles 30 June 2025 or has been remitted by the ATO.

Key points

- GIC and SIC incurred on or after 1 July 2025 are not deductible.

- The rule applies based on when the interest is incurred, not simply the tax year the debt relates to.

- GIC usually relates to late-paid tax debts and some unpaid tax amounts.

- SIC can apply when an amended assessment increases a tax liability.

- ATO interest should be tracked separately so your reports and tax workpapers do not overstate deductible expenses.

Main parts of the ATO interest change

| Part | What it means | Why it matters |

|---|---|---|

| General interest charge (GIC) | Interest the ATO can charge on late-paid tax debts and some unpaid amounts | It can keep accruing while a debt remains unpaid |

| Shortfall interest charge (SIC) | Interest that can apply when an amended assessment increases tax payable | It often appears after a tax return or assessment is corrected |

| 1 July 2025 cutover | GIC and SIC incurred on or after this date are not deductible | The date of incurrence drives the tax treatment |

| Remission | The ATO may reduce or cancel some interest in specific circumstances | A remitted pre-1 July 2025 amount may have tax consequences if it was previously deducted |

The ATO’s page on denying deductions for ATO interest charges says any GIC or SIC incurred on or after 1 July 2025 is not deductible, regardless of whether the debt relates to an earlier income year.

GIC compared with SIC

| Charge | Main question | Common trigger |

|---|---|---|

| GIC | Was tax or another ATO amount paid late or left unpaid? | A BAS, income tax, PAYG or other ATO debt remains outstanding |

| SIC | Did an amended assessment increase the tax payable? | A tax return is amended and the final liability is higher |

| Penalty | Was there a failure, false statement or other compliance issue? | Late lodgement, incorrect statement or other penalty event |

The labels matter because they do not all mean the same thing. Interest, penalties, tax payable, GST payable and PAYG instalments can sit close together in ATO accounts, but they may need different treatment in your bookkeeping and tax return.

Simple example

Imagine a small consulting company has an unpaid BAS amount from May 2025. The business enters a payment arrangement and pays the debt down over several months.

Any GIC incurred before 1 July 2025 may still be deductible, subject to the usual rules and adviser review. GIC incurred from 1 July 2025 onward is not deductible, even though the original BAS debt started before that date.

If the bookkeeper codes all interest to one generic “interest expense” account, the profit and loss may show a deductible-looking expense that needs adjustment later. A cleaner approach is to record ATO interest separately, keep the ATO statement, and make the tax treatment visible for the accountant.

What to check before relying on the deduction

Before treating any ATO interest amount as deductible or non-deductible, check:

- the date the GIC or SIC was incurred

- whether the amount is GIC, SIC, penalty, tax payable, GST, PAYG withholding or PAYG instalment

- whether any part of the charge was remitted by the ATO

- whether a pre-1 July 2025 deduction was already claimed in a prior tax return

- whether the business has an ATO payment arrangement or disputed assessment

- whether the amount is material enough to flag separately for your accountant

This is not a place for guesswork. If a charge straddles 30 June 2025, keep the ATO transaction detail and ask your adviser how to split the treatment.

How to use ATO interest in accounting software

In accounting software, the aim is not to make the tax call automatically. The aim is to keep the record clean enough that the tax call can be made correctly.

For Gimbla users, that usually means:

- keeping ATO payments separate from supplier bills and ordinary bank fees

- using a clear chart of accounts so ATO interest does not mix with loan interest

- reconciling the bank payment against the right ATO amount through bank reconciliation

- keeping BAS, GST, PAYG withholding and PAYG instalments distinct

- reviewing the Profit and Loss before tax time so non-deductible interest is not hidden in operating expenses

If the charge relates to GST or activity statement work, the BAS and IAS types guide and GST, VAT and sales tax guide can help you keep the surrounding tax accounts clearer.

Practical checklist

- Download or save the ATO statement showing the interest charge.

- Identify whether the amount is GIC, SIC, penalty, tax payable or another ATO amount.

- Note the incurred date and whether any part is before 1 July 2025.

- Code the payment to a separate ATO interest or tax-interest account rather than a generic expense account.

- Reconcile the bank transaction and attach the ATO evidence where your process allows.

- Give your accountant a short note before tax time if the amount is material or partly remitted.

- Review whether the underlying cash-flow issue needs a tax payment plan, BAS rhythm or monthly close improvement.

Frequently asked questions

Are ATO interest charges tax deductible?

GIC and SIC incurred on or after 1 July 2025 are not deductible. Amounts incurred before that date may still be deductible, depending on the facts and the year in which they were incurred.

What is the difference between GIC and SIC?

GIC usually applies to late-paid tax debts and some unpaid ATO amounts. SIC can apply when an amended assessment increases the amount of tax payable.

Should ATO interest be coded as a normal business expense?

Not automatically. From 1 July 2025, GIC and SIC should be tracked carefully because they are no longer deductible when incurred on or after that date. A separate account or clear note can make year-end review easier.

Can the ATO remit interest charges?

The ATO may remit interest in some circumstances, but businesses should not assume remission will apply. Keep the ATO notices, payment history and explanation for your adviser if you plan to request remission or have already received it.

Conclusion

The ATO interest change is simple to state but easy to mishandle in the books. From 1 July 2025, GIC and SIC are no longer deductible when incurred, so a late tax payment can affect cash flow without creating the same tax deduction it once did.

For small businesses, the safest habit is clean separation: tax payable in one place, PAYG and GST in their own accounts, ATO interest clearly identified, and unusual charges flagged before tax time. That gives your accountant the evidence they need and keeps the profit and loss from telling a misleading story.