- Overview

- Quick answer

- Key points

- Investing activities formula

- What counts as investing activities?

- Investing, operating and financing activities compared

- Simple example

- Negative investing cash flow is not always bad

- Positive investing cash flow needs context too

- Depreciation and investing cash flow

- Records to check before relying on the number

- How Gimbla can help

- Practical review checklist

- Frequently asked questions

- Conclusion

Investing Activities in Cash Flow: Examples and Formula

Published February 22nd, 2025 | Updated June 7th, 2026 | Team Gimbla

Investing activities in a cash flow statement are the cash movements from buying or selling long-term assets and investments. The section shows whether cash went into equipment, vehicles, fit-outs, property, major software, business acquisitions or similar assets, or came back from selling them.

For a small business, cash flow from investing activities helps answer a simple question: did cash leave the business because it is investing in future capacity, or did cash come in because assets were sold? Read it beside the cash flow statement, Profit and Loss, balance sheet, fixed asset register and bank records.

Investing cash flow is not the same as profit. It shows cash tied up in long-term assets, so it needs context before you treat a positive or negative number as good or bad.

Quick answer

Investing activities are the part of the cash flow statement that records cash movements from buying and selling long-term assets and other investments. Under the current AASB 107 Statement of Cash Flows compilation, investing activities are the acquisition and disposal of long-term assets and other investments that are not cash equivalents.

For small-business owners, the practical version is this: buying a work vehicle, replacing equipment, fitting out a shop or selling an old asset can affect investing cash flow. Ordinary trading income, wages, rent, GST payments and supplier bills usually sit elsewhere.

The simple formula is:

Cash received from selling long-term assets and investments - cash paid to buy long-term assets and investments = net cash flow from investing activities.

If you only need the short definition, use the Net Cash Flow From Investing Activities glossary. This guide explains how to read the number in context.

Key points

- Investing activities usually involve long-term assets, not daily operating costs.

- A negative investing cash flow can be normal when a business is buying equipment or expanding.

- A positive investing cash flow can mean assets were sold, which may be useful or may point to pressure.

- Depreciation is not a cash movement, even though it connects to the asset purchase later.

- The number is most useful when checked against operating cash flow, debt, cash reserves and the asset register.

Investing activities formula

The investing activities formula starts with cash proceeds from asset sales and investment disposals, then subtracts cash paid for long-term assets and investments.

For a small business, it often looks like this:

Asset sale proceeds - equipment purchases - vehicle purchases - fit-out purchases - other long-term asset purchases = net cash flow from investing activities.

A positive result means more investing cash came in than went out during the period. A negative result means more cash was used for long-term assets or investments than came back from disposals. Neither result is automatically good or bad until you compare it with operating cash flow, financing cash flow and the business reason for the asset decisions.

What counts as investing activities?

The investing section focuses on cash used for assets that are expected to help the business beyond the current period. It is not a bucket for every investment-like decision.

| Cash movement | Usually investing activity? | Why |

|---|---|---|

| Buying equipment, tools, vehicles or fit-out assets | Yes | These are long-term business assets |

| Selling a vehicle, machine, fit-out or other fixed asset | Yes | The business receives cash from disposing of a long-term asset |

| Buying major software or intangible assets | Often yes | It may create a recognised long-term asset |

| Buying and selling long-term investments | Often yes | It can be an investment outside daily operations |

| Paying wages, rent, subscriptions or suppliers | No | These are usually operating activities |

| Borrowing money or repaying principal on a loan | No | These are usually financing activities |

| Recording depreciation | No | Depreciation is non-cash; it allocates asset cost over time |

The key test is whether cash moved because the business acquired or disposed of a long-term asset or investment. AASB 107 also notes that only expenditures resulting in a recognised asset are eligible for classification as investing activities.

Investing, operating and financing activities compared

The cash flow statement separates cash movements into three broad sections.

| Section | What it explains | Common small-business examples |

|---|---|---|

| Operating activities | Cash from normal trading | customer receipts, supplier payments, wages, tax payments |

| Investing activities | Cash from long-term assets and investments | equipment purchases, asset sales, major fit-outs |

| Financing activities | Cash from funding the business | loans, repayments, owner contributions, dividends |

business.gov.au’s cash flow statement guide explains that a cash flow statement tracks money flowing in and out of the business so owners can identify payment cycles, forecast future finances and plan for shortages or surpluses.

That planning works better when the sections are not mixed together. A business that is short of cash because customers are late is in a different position from a business that used cash to buy productive equipment.

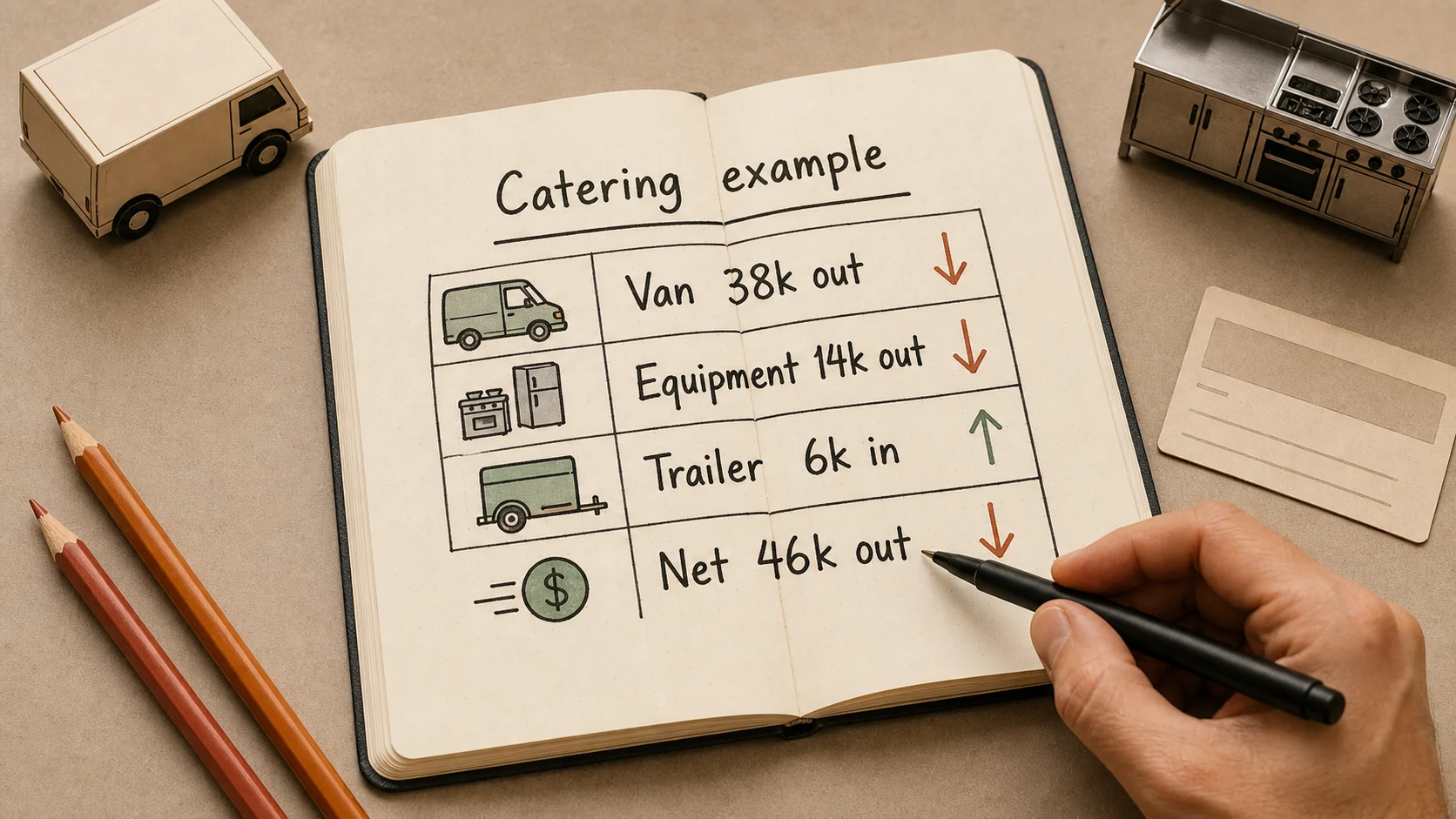

Simple example

A catering business reviews its cash flow statement for the year:

| Investing cash movement | Cash effect |

|---|---|

| Bought a delivery van | -$38,000 |

| Bought kitchen equipment | -$14,000 |

| Sold an old trailer | +$6,000 |

| Net cash flow from investing activities | -$46,000 |

The negative investing cash flow does not automatically mean the business is unhealthy. It means $46,000 more cash went into long-term assets than came back from asset sales.

The owner should then ask:

- Did operating cash flow stay positive?

- Were the purchases planned and affordable?

- Are the van and kitchen equipment recorded in the fixed asset register?

- Is depreciation set up correctly?

- Did any finance or loan repayments appear in the financing section instead of being mixed into investing cash flow?

Negative investing cash flow is not always bad

Negative investing cash flow often appears when a business is growing, replacing old assets or improving capacity. Examples include buying a vehicle, adding machinery, fitting out a new location or building a major system.

It becomes a concern when the spending is not supported by cash reserves, operating cash flow or realistic financing. A business can run into trouble if it buys assets while customer receipts are weak, supplier bills are overdue or debt repayments are already tight.

For this reason, read investing cash flow with:

- operating cash flow

- financing cash flow

- bank balances and reconciliations

- accounts receivable and accounts payable

- the balance sheet and asset register

Positive investing cash flow needs context too

Positive investing cash flow means more cash came in from investing activities than went out. That can happen when a business sells equipment, property, investments or another long-term asset.

That may be sensible if the asset was no longer needed, the business upgraded to a different model, or the sale funded a better plan. It may be a warning sign if the business is selling productive assets to cover ordinary bills.

The number itself does not tell you which story is true. The notes, asset records and management context matter.

Depreciation and investing cash flow

Asset purchases and depreciation often get confused.

When a business buys a long-term asset with cash, that cash movement may appear in investing activities. After that, the asset usually appears on the balance sheet and its cost may be spread over time through depreciation.

Depreciation affects the Profit and Loss statement and asset values, but it is not a cash payment. The cash left the business when the asset was bought, not each time depreciation is recorded.

That is why a business can have:

- a large investing cash outflow in the year it buys equipment

- depreciation expense across later periods

- a lower asset value on the balance sheet over time

For the practical accounting workflow, see the fixed asset depreciation guide and the depreciation user guide.

Records to check before relying on the number

Investing cash flow depends on clean records. Before using the report for decisions, check:

- major asset purchases were not coded to ordinary repairs or general expenses

- asset sales were recorded with the sale proceeds and any disposal entries

- GST treatment was reviewed where relevant

- loans and repayments were not mixed into asset purchase lines

- depreciation entries did not get treated as cash movements

- the fixed asset register agrees with the balance sheet

- bank transactions were reconciled to the right bills, receipts and journals

These checks help avoid a misleading report. For example, coding a new vehicle to repairs can make operating expenses look too high and investing cash flow look too low.

How Gimbla can help

In Gimbla, investing cash flow becomes easier to review when asset purchases, supplier bills, bank payments and journals are connected. A tidy workflow usually looks like this:

- Record the supplier bill or payment for the asset.

- Match the bank transaction during bank reconciliation.

- Add the asset to the right balance sheet account and fixed asset records.

- Set up depreciation if the asset needs to be depreciated.

- Review the Profit and Loss, balance sheet and cash flow statement together.

The goal is not just a correct report. It is a clearer trail from the cash movement to the asset, depreciation and management decision behind it.

Practical review checklist

Use this checklist when investing cash flow looks unusually high, low, positive or negative:

- List the biggest asset purchases and asset sales for the period.

- Compare each item with bank transactions and supplier or sale documents.

- Check whether the asset is still in use.

- Confirm whether the transaction belongs in investing, operating or financing activities.

- Compare the result with operating cash flow and loan repayments.

- Ask whether the spending supports the next 12 months of trading.

- Note any records your accountant needs before year end.

Frequently asked questions

What are investing activities in cash flow?

Investing activities are cash movements from buying or selling long-term assets and investments. In a small business, common examples include equipment purchases, vehicle sales, fit-outs and major software assets.

Is negative cash flow from investing activities bad?

Not always. It can be normal when a business buys equipment, vehicles or other long-term assets. It needs context from operating cash flow, financing cash flow, cash reserves and the business plan.

Does depreciation appear in investing cash flow?

Depreciation is not a cash movement. The asset purchase may appear in investing cash flow, while depreciation affects the Profit and Loss and balance sheet over time.

Are loan repayments investing activities?

No. Loan repayments are usually financing activities. The asset purchase may be an investing activity, while the borrowing and repayment sit in the financing section.

Conclusion

Cash flow from investing activities shows how cash moved through long-term asset decisions. For a small business, it helps explain equipment purchases, asset sales, fit-outs, major software and other investments that shape future capacity.

Read the number with context. A negative result may show growth investment. A positive result may show a planned asset sale. The useful question is not whether the number is positive or negative, but whether the cash movement matches the business plan and the records behind it.